Section I: U.T. System Debt Overview | |||||||||

| Q1: | What is the Revenue Financing System (RFS)? | ||||||||

| A1: | The Revenue Financing System (RFS) is a cost-effective debt program secured by a system-wide pledge of all legally available revenues for debt issued on behalf of all 13 institutions and System Administration. The RFS is governed by a master resolution and supplementing resolution authorized periodically by the Board. | ||||||||

| Q2: | What is the RFS Commercial Paper (CP) program? | ||||||||

| A2: | The RFS CP Program is a pooled financing program used to provide interim financing for capital improvements and to finance equipment purchases. TRB CP is issued as part of the overall RFS CP program. All equipment purchases are financed via the RFS CP program. Most Capital Improvement Program (CIP) projects are initially financed through the program until they are fixed out into long-term bonds. | ||||||||

| Q3: | What are Tuition Revenue Bonds (TRBs)? | ||||||||

| A3: | Tuition Revenue Bonds (TRBs) are issued under the RFS program and are secured by the same pledge of all legally available revenues of the System; however, the expectation is that the State will reimburse TRB debt service with general revenue. Despite the name, TRB debt service is not necessarily paid from tuition and fees. In fact, an institution is not required to have tuition in order to be eligible for TRB debt proceeds. Tuition Revenue Bond debt is specifically authorized by the Legislature under Ch. 55 of the Education Code. Please see Ch. 55 of the Education Code for further detail regarding this topic. | ||||||||

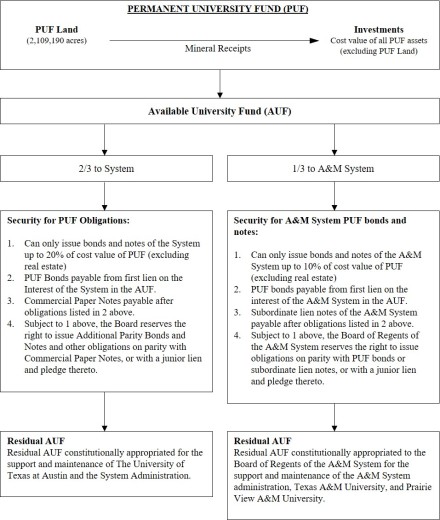

| Q4: | What is the Permanent University Fund (PUF)? | ||||||||

| A4: | The Permanent University Fund (PUF) is a constitutional fund and public endowment created in the Texas Constitution of 1876. The PUF debt program is used to fund E&G projects at System institutions plus System Administration. PUF debt is secured by distributions from the PUF to the Available University Fund (AUF). The AUF is shared by U.T. System and Texas A&M System as outlined below:

| ||||||||

| Q5: | Can PUF debt be used to fund auxiliary projects? | ||||||||

| A5: | No, Article 7, Section 18(d) of The Texas Constitution states that the proceeds of the bonds or notes issued under Subsection (a) or (b) of this section may not be used for the purpose of constructing, equipping, repairing, or rehabilitating buildings or other permanent improvements that are to be used for student housing, intercollegiate athletics, or auxiliary enterprises. | ||||||||

| Q6: | How is U.T. System authorized to issue debt? | ||||||||

| A6: | U.T. System has both constitutional and statutory authorization to issue debt. Please see the following links regarding U.T. System’s authorization for the issuance of debt: | ||||||||

| Q7: | What are U.T. System’s credit ratings? | ||||||||

| A7: | All U.T. System debt programs bear credit ratings from Moody’s, Standard & Poor’s and Fitch for both long-term and short-term debt. ● The current long-term debt ratings for both PUF and RFS are: Moody’s: Aaa S&P: AAA Fitch: AAA ● The current short-term debt ratings for both PUF and RFS debt are: Moody’s: P-1/VMIG1 S&P: A-1+/A-1+ Fitch: F-1+/F1+ These ratings represent the highest possible rating levels from all three rating agencies for both long-term and short-term debt. | ||||||||

Section II: Debt Approval Process | |||||||||

| Q8: | What is the approval process for debt funded projects? | ||||||||

| A8: | Please refer to Policy UTS168. | ||||||||

| Q9: | What is the “Finding of Fact?” | ||||||||

| A9: | The Master Resolution establishing the Revenue Financing System requires that before any RFS debt is issued, the BOR must make a determination that:

The Office of Finance makes these two determinations on behalf of the BOR by analyzing debt capacity, and that is called the “Finding of Fact.” Finding of Fact is required before the BOR can grant DD approval for any RFS or TRB funded project. | ||||||||

| Q10: | What are “Pledged Revenues?” | ||||||||

| A10: | Under the Master Resolution, the Board has, with certain exceptions, combined all of the revenues, funds and balances, attributable to Members of the RFS and lawfully available to secure revenue-supported indebtedness into a system-wide pledge to secure the payment of Parity Debt from time to time issued under the Master Resolution. Pledged Revenues do not include: (a) the interest of U.T. System in the AUF; (b) funds held in the Permanent Health Fund and amounts distributed to any member from the Permanent Health Fund; (c) amounts appropriated to any Member from the HEAF; (d) except to the extent so appropriated, general revenue funds appropriated to U.T. System by the State; and (e) Practice Plan Funds of any Member, including the income from and any fund balances related thereto not included in Pledged Practice Plan Funds. Pledged Revenues not utilized to pay debt service on Parity Debt are available to pay other costs of operating the University System. | ||||||||

| Q11: | What is my institution’s debt capacity, and what impact will a particular project have on debt capacity? | ||||||||

| A11: | A particular project’s impact to an institution’s debt capacity will depend on its impact to the institution’s overall forecast. Assuming that the project is non-revenue generating, an institution must meet or exceed at least two of the three following credit ratios:

Please note that the Office of Finance believes debt capacity is both a quantitative and qualitative concept and cannot be determined by formulas and ratios alone; however, these standards serve as the foundation for determining access to RFS debt. | ||||||||

| Q12: | What if my project is revenue-generating? | ||||||||

| A12: | The standard for a revenue-generating project is 1.3x coverage (exclusive of depreciation). If the project is non-revenue generating (i.e., not self-supported), the Office of Finance defers to the institution’s debt capacity ratios. | ||||||||

| Q13: | My institution is interested in taking out a capital lease. Since this action would not be part of any U.T. System debt program, can I take out a capital lease without any authorizations? | ||||||||

| A13: | THECB and BRB approval is not required for capital leases. However, Board of Regents (BOR) approval is required prior to entering into any contract in excess of $1,000,000. | ||||||||

Section III: Debt Issuance and Management | |||||||||

| Q14: | Which funds should be spent first if a project has multiple funding sources? | ||||||||

| A14: | The appropriate order of funding is generally TRB, PUF, RFS and then local funds. | ||||||||

| Q15: | How often does the Office of Finance issue CP, what determines a project’s eligibility for CP issuance, and how is the issuance amount determined? | ||||||||

| A15: | RFS CP issuances are generally done on a quarterly basis, each November, February, May, and August. A project’s eligibility for CP issuance is based on the following factors:

The institution determines the issuance amount by analyzing projected cash flows which are available from the project managers and/or OFPC. | ||||||||

| Q16: | What is “arbitrage”, and what are the IRS spend-down rules related to tax-exempt proceeds? | ||||||||

| A16: | Arbitrage refers to the act of issuing debt at relatively low tax-exempt rates then investing the proceeds at higher taxable rates. Tax-exempt borrowing is a privilege, and the IRS maintains that arbitrage is an abuse of that privilege. The IRS regulates against arbitrage by enforcing spend-down rules for all tax-exempt debt proceeds. The spend-down rules are an important consideration when determining how much debt to issue for a project. Spend-down schedules are determined by the percentage of proceeds to be used on equipment.

Note: There is no penalty against spending down faster than the required schedule. | ||||||||

| Q17: | How soon do debt proceeds become available for reimbursement? | ||||||||

| A17: | Debt proceeds usually become available within one day of issuance. | ||||||||

| Q18: | What are the rules on private use, and how do they affect the type of debt (taxable vs. tax-exempt) issued? | ||||||||

| A18: | Because we are a public institution, the government allows us to borrow money (issue debt) at tax-exempt rates, which are generally lower than the taxable rates at which corporate entities borrow. In exchange for that privilege, the government expects us to utilize the vast majority of our facilities for tax-exempt public purposes. However, it is not uncommon to have some small amount of private activity going on inside a building, such as the granting of naming rights, contracts for the provision of dining services, and management contracts. If a project has more than the allowable amount of private use, it is possible that it will need to be financed with taxable debt. Please see the Private Use Guidelines memo on the Office of Finance webpage for detailed parameters covering management contracts and naming rights. | ||||||||

| Q19: | When do equipment financing reimbursements and equipment pay downs occur? | ||||||||

| A19: | Equipment is reimbursed on a quarterly basis (each November, February, May, and August) as part of the quarterly RFS CP issuance. Equipment pay downs occur twice a year in February and August. | ||||||||

| Q20: | What are the guidelines for equipment financing reimbursement requests? | ||||||||

| A20: | The minimum amount of equipment to be financed for any institution is $100,000 per funding with smaller equipment purchases allowed to be bundled together to reach the minimum of $100,000. The equipment must also have a useful life equal to or greater than three years. The amortization period for equipment financing ranges from 3-10 years depending on the useful life of the equipment financed. For further information regarding the Equipment Financing Program history, rules, and procedures, please see the complete guidelines here. | ||||||||

Section IV: Debt Budgeting and Forecasting | |||||||||

| Q21: | Who should I contact with questions regarding the debt budget? | ||||||||

| A21: | Although the Office of Finance works in conjunction with the Office of the Controller during budget session, any debt budget-related questions should be directed to Robin Webb in the Office of Finance, as we track debt by project by institution. | ||||||||

Section V: Cash Management | |||||||||

| Q22: | When are construction reimbursements transferred to the institutions? | ||||||||

| A22: | Construction reimbursements are transferred monthly. Deadlines to transmit the required accounting documentation to the Office of Capital Projects is generally around the 14th of the month, and the reimbursement date is typically on the 20th, but the exact dates will be communicated annually. | ||||||||

| Q23: | How do I communicate transactions I wish to initiate related to the STF and ITF? How can I monitor balances, daily activity and generate reports? | ||||||||

| A23: | Institutions will use the Client Participation System (CPS) to transfer cash to and from the STF and to purchase or sell units of the ITF. Transactions include inbound wire transfers to the STF, outbound wire transfers from the STF, transfers between institutions as well as monthly rebalancing transactions between the STF and ITF. The CPS website will not be accessible from the UTIMCO website to minimize any casual traffic. UTIMCO will provide a link and a login ID to authorized users. CPS is intended for transaction processing only. Institutions can use CPS to schedule STF transactions for any business day, even weeks in advance. ITF transactions (purchases and redemptions) are permitted on the first business day of each month. Institutions will use Component Reports to monitor balances and daily transaction activity. Components Reports can also be used to generate reports to review transactions, historical account balances, ITF prices and STF yields. The Component Reports application is accessible from the UTIMCO website. For more information about centralization, please contact the U.T. System Office of Finance. | ||||||||